Part 2 of a Series on Insurance Core Platforms and Modernization

How Policy Logic Becomes A Memory and Why Insurance Cannot Let It Go

Most people meet OIPA at the wrong moment. They encounter it when a product launch slows down, when a regulatory change triggers weeks of discussion, or when a modernization initiative suddenly feels heavier than expected. By the time OIPA becomes visible, it already contains years of decisions that no one clearly remembers making.

This is not a flaw in the system. It is the result of how insurance works and how OIPA was designed to support it. Insurance does not reset easily. Promises made in the past continue to matter long after the teams and technologies that created them have moved on.

In the first part of this series, we explored why OIPA still runs insurance and why replacing it rarely works the way transformation roadmaps suggest. This second part goes deeper into the system itself. It explains how OIPA actually works, why it feels heavy, and why that heaviness is often necessary rather than accidental.

To understand OIPA clearly, it helps to stop thinking of it as an application and start thinking of it as a memory system for long-term financial obligations.

Access the Part 1 article here: OIPA VS Modern Insurance Core Platforms

What OIPA Represents Inside an Insurer

OIPA is usually described as a policy administration system, but that label hides its true role. OIPA is not simply where policies are stored or processed. It is where an insurer defines what truth means when time passes and conditions change.

A policy is not a static object. It is a living agreement that unfolds over years or decades. Premiums change. Coverage terms evolve. Regulations intervene. Customer behavior shifts. OIPA exists to ensure that these changes never contradict the original promise made at issuance.

Because of this responsibility, OIPA prioritizes consistency over flexibility. It enforces continuity even when business intent evolves. When teams feel resistance from the system, what they are often experiencing is protection of historical commitments rather than technical limitation.

OIPA feels heavy because it carries institutional memory, not because it is inefficient.

The Mental Model OIPA Enforces

Many modern systems are built around a request-response mindset. A request arrives, logic executes, and a response is returned. Once the response is delivered, the system often forgets the context.

OIPA does not operate this way. OIPA thinks in timelines.

Every policy moves through a defined lifecycle. Each action is evaluated not only for correctness in the present moment, but also for compatibility with past and future states. Changes are never isolated. They are contextualized within a sequence of events.

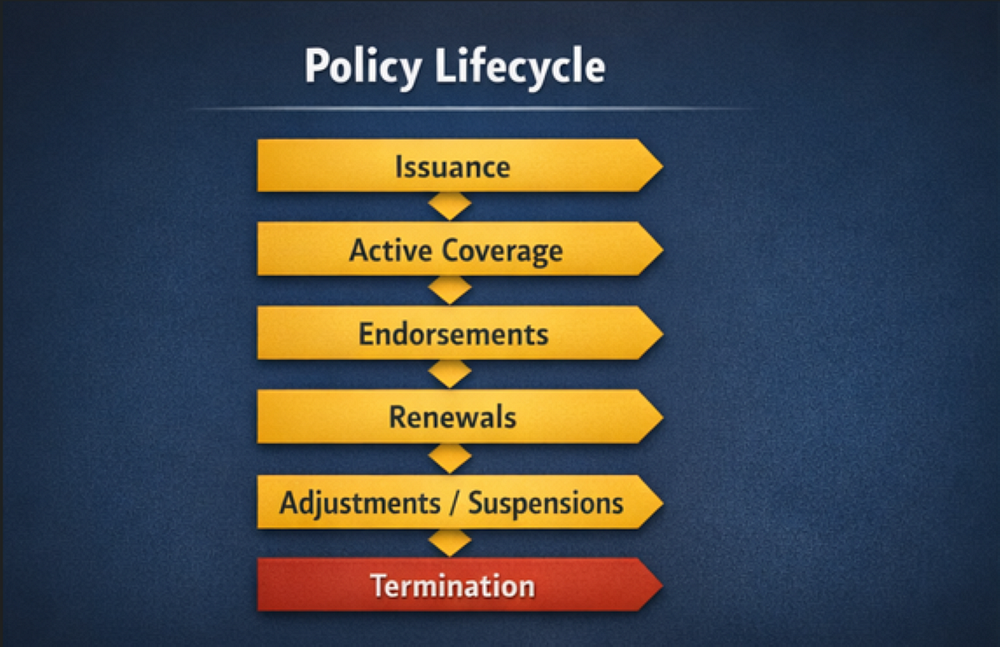

A simplified view of how OIPA models a policy looks like this.

Each stage has financial consequences. Each consequence must reconcile with earlier assumptions. OIPA exists to ensure that these reconciliations remain consistent across time.

This mindset is difficult for teams accustomed to stateless services, but it is fundamental to insurance.

Why Configuration Sits at the Center of OIPA

OIPA is deeply configuration driven. This design allows insurers to define products, rules, and calculations without writing application code for every change. On the surface, this appears to offer flexibility and control.

In practice, configuration becomes a form of programming.

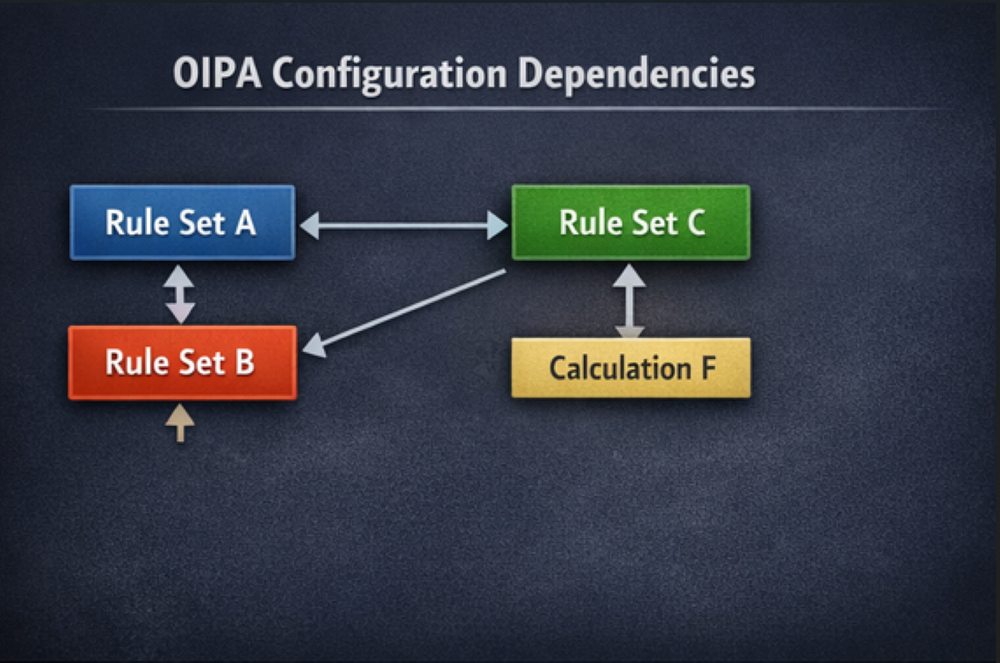

Rules reference other rules. Calculations depend on conditions defined elsewhere. Exceptions accumulate as products evolve. Over time, configuration grows more complex without being refactored.

A mature OIPA configuration often resembles a dependency network rather than a clean hierarchy.

No single team designed this structure. It emerged gradually as the business responded to new requirements. That emergence is why OIPA configurations contain institutional memory. It is also why replacing them is risky.

You are not just rewriting logic. You are rewriting history.

When Configuration Starts Working Against Teams

Configuration works well when products are stable and changes are incremental. Problems appear when change accelerates.

A small pricing update touches logic written years earlier. A regulatory requirement conflicts with an old exception. A new product variant behaves correctly in isolation but incorrectly when combined with existing offerings.

At this stage, teams realize that OIPA behaves less like a flexible system and more like a constitution. Amendments are possible, but they require careful review. Large rewrites carry risk that extends beyond the immediate change.

Delivery slows not because OIPA is inefficient, but because the consequences of mistakes are long-lived.

A Realistic Implementation Scenario

In one insurer, a minor adjustment to premium rounding rules caused discrepancies in long-running policies. The updated logic was correct. The math was sound. Test cases passed without issue.

The problem was temporal rather than technical.

Policies issued years earlier were based on assumptions that no longer applied. OIPA enforced continuity rather than intent. The business wanted forward correction. The system demanded respect for historical commitments.

The release was delayed for months while teams reconciled present expectations with past promises. No defect existed. The delay was the cost of consistency.

This type of scenario is common in OIPA implementations and rarely visible in planning documents.

Why OIPA Feels Slow Even When It Is Not

OIPA is frequently described as slow, but this label often misidentifies the source of delay. Most delays occur outside the system rather than inside it.

Governance layers surround OIPA because changes carry long-term risk. Configuration updates require review. Regression testing expands. Sign-offs multiply. These processes exist because OIPA changes do not fail quickly or obviously.

A misconfigured rule may not cause an immediate outage. It may quietly affect policies over months or years. That risk shapes organizational behavior.

Teams slow down because being wrong is more expensive than being slow.

The Cloud Question and Its Limits

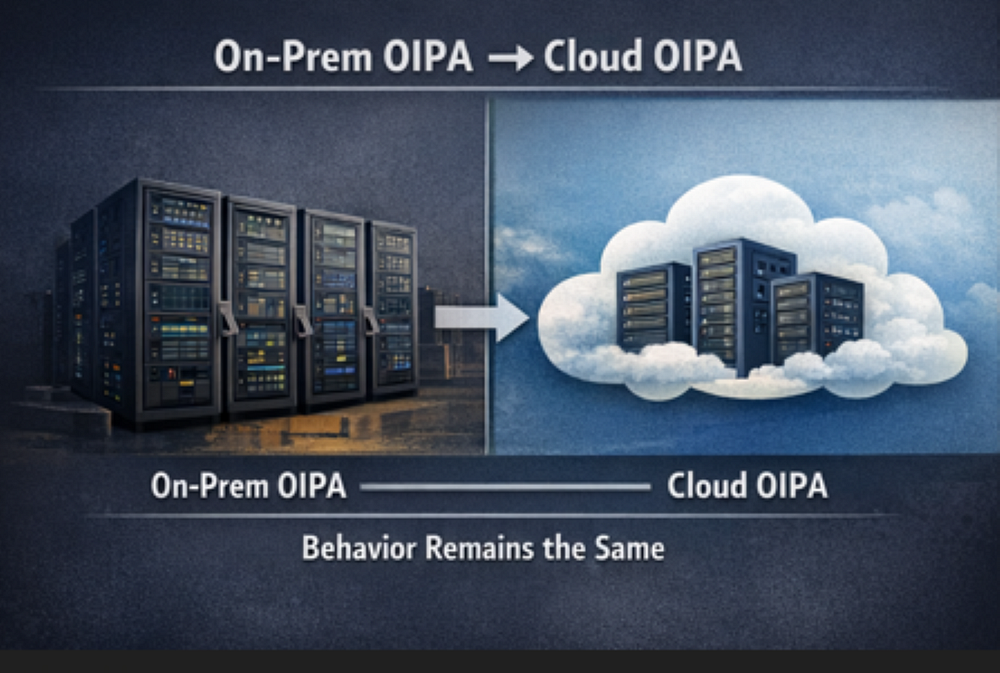

OIPA can run in cloud environments, and many insurers have already moved it there. Cloud infrastructure improves resilience, scalability, and operational visibility.

What cloud does not automatically change is behavior.

OIPA still expects deliberate change. It still rewards stability. It still assumes that correctness outweighs experimentation. Cloud hosting changes where OIPA runs, not why it exists.

This distinction becomes clear when simplified.

Cloud enables better operations, but it does not rewrite the system’s philosophy.

The Architecture Insurers Actually End Up With

Despite early replacement ambitions, most insurers do not remove OIPA. They insulate it.

Over time, a common architecture emerges, even if it was not planned initially.

Modern layers absorb volatility. OIPA remains protected. Innovation occurs at the edges, while policy truth stays centralized.

This architecture is not elegant, but it aligns with how insurance manages risk.

The Human Cost of OIPA Complexity

When OIPA programs struggle, the root cause is rarely technology. It is organizational.

Configuration becomes dense. Documentation falls behind reality. Expertise concentrates in a small number of individuals. Over time, teams hesitate to change logic they do not fully understand.

Fear replaces confidence. Reviews become defensive. Innovation slows.

OIPA does not create these dynamics. It exposes them.

Why Replacement Eventually Feels Unrealistic

Early in modernization programs, replacement feels clean and decisive. Over time, it feels increasingly unrealistic.

Replacing OIPA means recreating policy truth elsewhere. That truth includes exceptions, regulatory interpretations, historical compromises, and edge cases that no one fully remembers designing.

Eventually, architects stop asking how to remove OIPA and start asking how to design around it without breaking what it protects.

That shift marks maturity rather than failure.

What OIPA Reveals About Insurance

OIPA reflects a deeper truth about insurance itself. Insurance is not fast by nature. It is deliberate.

The system mirrors the industry more than the industry mirrors the system. Trying to force OIPA into startup-style behavior misunderstands both.

Modernization succeeds when it respects this reality rather than fighting it.

Where Modernization Actually Works

Successful programs stop treating OIPA as a bottleneck. They treat it as a boundary.

They move quickly where speed is safe. They slow down where correctness matters. They accept coexistence rather than chasing purity.

This balance is difficult, but it is realistic.

About This Series

This article is the second part of a broader series examining insurance core platforms and the realities of modernizing them at scale. The upcoming pieces will explore common transformation patterns, the structural reasons many core system initiatives struggle, and how insurers approach change when policy integrity and long-term obligations cannot be compromised.

This was Part 2 of the MayhemCode Insurance series, following Part -1 on OIPA VS Modern Core Insurance Platforms.

Staying Ahead of Structural Reality

If this article felt slightly uncomfortable, that reaction is worth paying attention to. Discomfort often signals that long-held assumptions are being challenged, especially around systems that are expected to change without breaking the promises they carry.

The next part of this series will move beyond how OIPA works and examine why many core system initiatives struggle once replacement becomes the stated goal. The focus will be on real transformation patterns, common missteps, and how insurers balance ambition with the realities of policy truth, regulation, and long-term obligation.