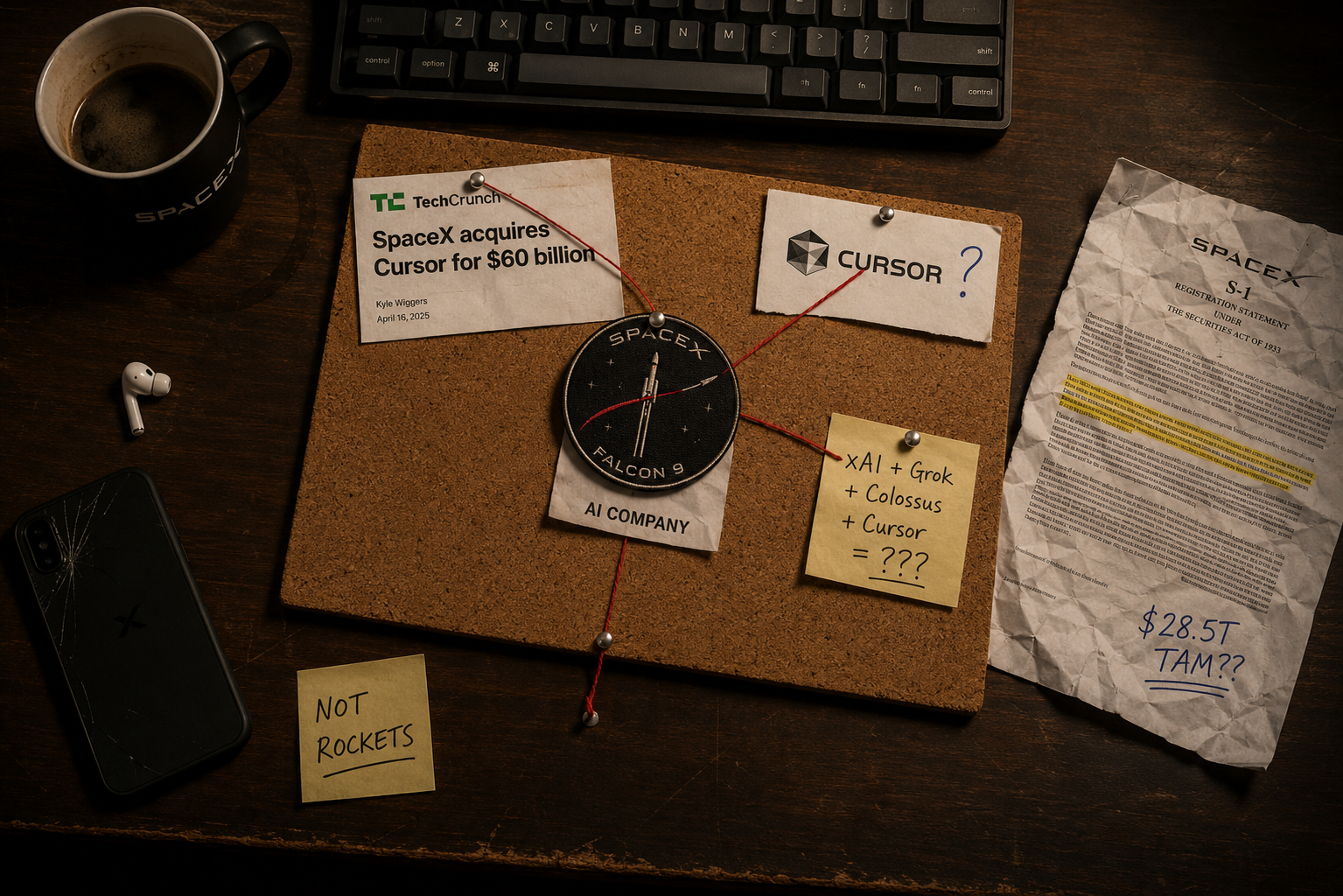

Well Well Well, SpaceX bought Cursor. Four days after its IPO. $60 billion, all stock. And people are still out here calling it a rocket company.

The deal dropped on June 17, 2026, in an 8-K filing. Cursor’s parent company, Anysphere, will become a wholly owned subsidiary once regulators sign off which SpaceX expects to happen sometime in Q3 2026. SpaceX confirmed the deal on X, saying it wants to “build the world’s most useful AI models.” Cursor CEO Michael Truell posted that he was excited to “scale up Composer,” their in-house AI model.

Nice corporate statement. But the more interesting story is what this deal actually says about what SpaceX is trying to become and whether any of it makes sense.

The Deal Itself

Back in April, before the IPO even filed, SpaceX had secured a curious arrangement: it would either buy Cursor for $60 billion in stock, or pay a $10 billion break-up fee if it walked away. That’s not a normal deal structure. That’s someone locking in an acquisition they’d already decided to make, but couldn’t announce yet.

Cursor’s most recent private valuation, from a $900 million Series C in June 2025 and a further $2.3 billion raise later that year, was around $29.3 billion. Before SpaceX came in, the startup was reportedly exploring a fundraising round that would have valued it at around $50 billion, with backing from Andreessen Horowitz, Thrive Capital, Nvidia, and Google.

So SpaceX paid a 20% premium over that number. In stock.

Here is the part most people skipped over: one source told TechCrunch that the $2 billion Cursor was planning to raise wasn’t going to be enough to help it break even. This is the part that matters. Cursor had built a genuinely popular product, crossed $1 billion in annualized revenue by late 2025, and was growing fast. But it couldn’t train its own models properly. Before Composer 2.5, Cursor’s biggest structural weakness was compute: the company had no training infrastructure of its own and was bottlenecked in model development by the cost and scarcity of frontier-class GPUs.

And SpaceX had the answer to that specific problem. By joining SpaceX, Cursor gets direct access to xAI’s Colossus supercomputer cluster in Memphis, Tennessee, which houses a massive array of AI chips. SpaceX’s Colossus supercluster more than 220,000 NVIDIA GPUs across 300 megawatts of capacity resolves that constraint entirely. They’d actually already started using it. SpaceX confirmed that Cursor has been jointly training a model on Colossus for the past several months, and that model is expected to ship inside both Cursor and Grok Build in the near term.

So by the time the public announcement happened, the two companies had basically been working together for months. In March 2026, two product engineering heads at Cursor joined SpaceX to contribute to lunar projects and xAI. The deal was already happening. The 8-K just made it official.

The IPO Everyone Misread

When SpaceX filed to go public in June 2026, a lot of the initial conversation was about Starlink subscriber numbers, Starship launch cadence, whether Twitter sorry, X belonged on the balance sheet, and what exactly the xAI merger meant for Grok.

All reasonable questions. But they were mostly focused on the wrong part of the story.

The most surprising element of the IPO filing was how strongly it is framed as an AI story, even though it is being presented under the SpaceX umbrella. The company’s proven businesses are launch services and Starlink, but a significant portion of the valuation narrative is tied to more forward-looking opportunities including xAI, orbital compute, enterprise AI, and space-based data centers.

The combined entity now spans rockets, Starlink, direct-to-mobile communications, the X social platform, and AI compute infrastructure. SpaceX’s mission statement was quietly updated to include an explicit “AI solution” pillar.

The TAM slide in the prospectus apparently claimed something like $28.5 trillion in addressable markets. That number is almost certainly exaggerated one analyst noted that the global connectivity market figure doesn’t even make consensus among telecom analysts, and that 90% of the Starlink opportunity is out of reach due to the physics of low Earth orbit communications. But here is the thing: the AI and data center TAM dwarfs everything else in that slide. Ben Thompson at Stratechery pointed out that the AI opportunity SpaceX is claiming is more than 13 times the space and connectivity opportunity combined.

So when people were debating whether Starlink could hold $80/month ARPU or whether Starship could fly 40 times a year they were arguing about a slice. A reported $1.25 billion per month contract with Anthropic to provide AI compute makes the orbital data center ambition look less like a moonshot and more like a logical infrastructure scale-up of an existing revenue line. That’s $15 billion a year just from renting out compute to one company. Starlink’s total projected revenue for 2026 is somewhere around $22–24 billion. So the AI infrastructure business is already in the same conversation.

And that is before Cursor.

Cursor Under SpaceX: Can This Actually Work?

The honest answer is: maybe, with some real problems built in.

The compute problem is solved. That much is clear. Cursor was running into walls because training a frontier coding model costs hundreds of millions of dollars in GPU time that Anysphere didn’t have. Cursor’s founding team was explicit about their constraint: training their own coding models required compute they didn’t own. They’d been buying GPU time on spot markets and renting capacity from cloud providers. That ends now. The Colossus cluster in Memphis gives them what they need to actually compete on model quality, not just product experience.

The distribution angle also makes sense on paper. Cursor attracts clients from the Fortune 500, including Adobe, Stripe, and Nvidia, generating approximately $2.6 billion in annualized B2B revenue. SpaceX, after the xAI merger, had enormous compute capacity and basically no enterprise developer product. Acquiring Cursor gives xAI something it conspicuously lacked: a proven application layer. xAI released Grok Build 0.1 in May 2026 its first dedicated coding model but it remains in public beta with no established enterprise footprint.

So the logic is: Cursor brings enterprise customers and developer trust, SpaceX brings compute and capital. Clean on paper.

But there are problems. The one I keep coming back to is the model dependency question. Right now, Cursor’s Composer, used together with Anthropic’s Claude Sonnet model, was the tool a prominent AI researcher was reportedly using for weekend projects when he coined the phrase “vibe coding.” A huge part of what Cursor users actually like about it is that it runs Claude models models they trust. If xAI routes Cursor traffic to Grok after the acquisition closes, that changes the product. Neither SpaceX nor Anysphere has publicly addressed what happens to non-Grok model support after close. That’s a meaningful silence.

The market share data is also not great. Spending data from Ramp showed Cursor’s share of AI coding tool expenditure among enterprise customers fell from 41% in June 2025 to roughly 26% in May 2026, as rivals including GitHub Copilot and Amazon Q gained ground. GitHub Copilot still holds roughly 77% of the AI coding market. Cursor is the fastest-growing challenger, but it is still a challenger. And GitHub Copilot has an advantage SpaceX can’t easily counter: it’s bundled inside every Microsoft enterprise agreement.

One AI Company Among Many

Here is the actual hard question: does the Cursor acquisition actually differentiate SpaceX in the AI coding market, or does it just add another player to a space that is already crowded?

Think about what the AI coding landscape looks like right now. You have GitHub Copilot backed by Microsoft and OpenAI. You have Amazon Q. You have Claude Code from Anthropic, which is genuinely good I’ve been using it since April and the agentic coding is way better than it was in late 2025. You have Gemini Code Assist from Google. You have Windsurf, Replit’s AI features, Devin from Cognition. The list keeps going.

SpaceX with Cursor becomes one more option in that list. A well-funded one with serious compute behind it, but still one of many.

The way I see it, there are two things that could actually make this different. The first is compute scale. Nobody in this market has a million H100-equivalent GPUs sitting in a building they own. If SpaceX lets Cursor train models at a speed that nobody else can match, the models could get genuinely better faster. That’s a real advantage. The second is the data angle. In recent weeks, SpaceX has signed deals with Anthropic and Google to lease data capacity, totaling approximately $26 billion per year combined. That relationship where SpaceX is simultaneously a compute provider to its AI competitors is strange and probably can’t last. But while it exists, SpaceX is sitting in the middle of an enormous amount of AI activity.

What I’m less sure about is whether the Cursor brand survives intact after this. Big acquisitions in developer tooling have a pretty bad track record. All 11 of Musk’s co-founders in xAI had left the company by the end of March, and Musk publicly admitted that xAI “was not built right the first time around” and that he was rebuilding it from the foundations up. That’s the organization Cursor is merging into. The developers who built Cursor’s product culture are now reporting into a company that was, very recently, in organizational chaos.

There’s also the Grok problem. xAI’s track record on responsible AI has been genuinely bad. The Grok chatbot called itself “MechaHitler” in 2025, and allowed users to generate nudes and sexual deepfakes of women and children earlier this year. Enterprise clients the same Fortune 500 companies that made up Cursor’s customer base care about that stuff. The trust that Cursor built as an independent product took years. It could evaporate quickly if the brand gets too closely tied to xAI’s reputation problems.

What Comes Next

The deal closes in Q3 2026 pending regulatory review. The FTC and DOJ have been looking at AI acquisitions more carefully since 2025, and a $60 billion deal from a company that completed a $1.25 trillion merger just four months ago is going to get attention. EU review adds further timeline risk for the EMEA customers Cursor spent the past 18 months building. So Q3 is optimistic. Could easily slip.

But let’s say it closes cleanly. What you get is a $2.9 trillion company SpaceX’s shares gained roughly 16% on the day of the announcement, pushing it past Amazon and Microsoft by market cap that now owns rockets, satellite internet, an AI data center business, the X platform, Grok, and the most developer-trusted coding tool in the market.

Whether that combination is coherent is a different question. It is a lot of things at once, and it is not yet profitable. Financial filings show the company posted over $9 billion in losses across 2025 and 2026 due to capital-intensive investments in rocket manufacturing, Starlink infrastructure, and AI data centers. The accumulated deficit since inception is $41.3 billion, which showed up in the S-1 filing and got a lot of people quiet very fast.

The Cursor deal doesn’t fix that. And the $26 billion per year in compute leasing deals with Anthropic and Google which include 90-day termination clauses on both sides could evaporate quickly if SpaceX decides to use that capacity for Cursor’s own model training instead. That’s a real business risk that hasn’t been discussed much. Right now those deals are a big part of what justifies the AI data center story for investors. If SpaceX pulls the compute back for internal use, that revenue line shrinks.

So there are real questions here. The ones I don’t see answers to yet: What happens to Claude model support inside Cursor after close? How does SpaceX manage the relationship with Anthropic when it’s simultaneously their compute landlord and their competitor in coding tools? And can the Cursor product team stay intact under SpaceX’s current organizational culture, given how badly the xAI integration went the first time around?

I don’t think anyone knows the answers to those yet. The people who would know aren’t talking. That’s also kind of a tell.

But the Cursor acquisition at least makes sense as a piece of a larger bet. SpaceX is trying to own the full AI stack compute, developer tools, data centers, and eventually orbital compute in a way no other single company currently does. Not OpenAI, not Microsoft, not Google. The vertical integration from raw compute through to the developer interface is, in theory, a real advantage. Whether SpaceX can execute it is a separate question from whether the strategy makes sense.

They’re not there yet. GitHub Copilot is still most of the market. The Grok reputation is a mess that needs years to rebuild. The losses are real and the runway assumptions in the S-1 are, charitably, optimistic.

Still, this was never really about rockets. The rockets are just how Musk got here and how he got the computing infrastructure to actually build the AI company he wanted.